More Startups. Fewer Jobs.

In 2010, the Kauffman Foundation published one of the most influential findings in modern entrepreneurship policy: Startups were responsible for all net new job creation in the American economy.

That paper became the intellectual foundation for a generation of startup ecosystem building. Accelerators. Innovation districts. Venture funds. Pitch competitions. University incubators. Entrepreneurship centers. State startup offices. Over $1 Trillion invested across the nation.

The logic was simple and compelling: More startups → more jobs → more economic growth.

So for the last fifteen years, we built the machine. And in many ways, it worked. America today is experiencing a sustained surge in entrepreneurship.

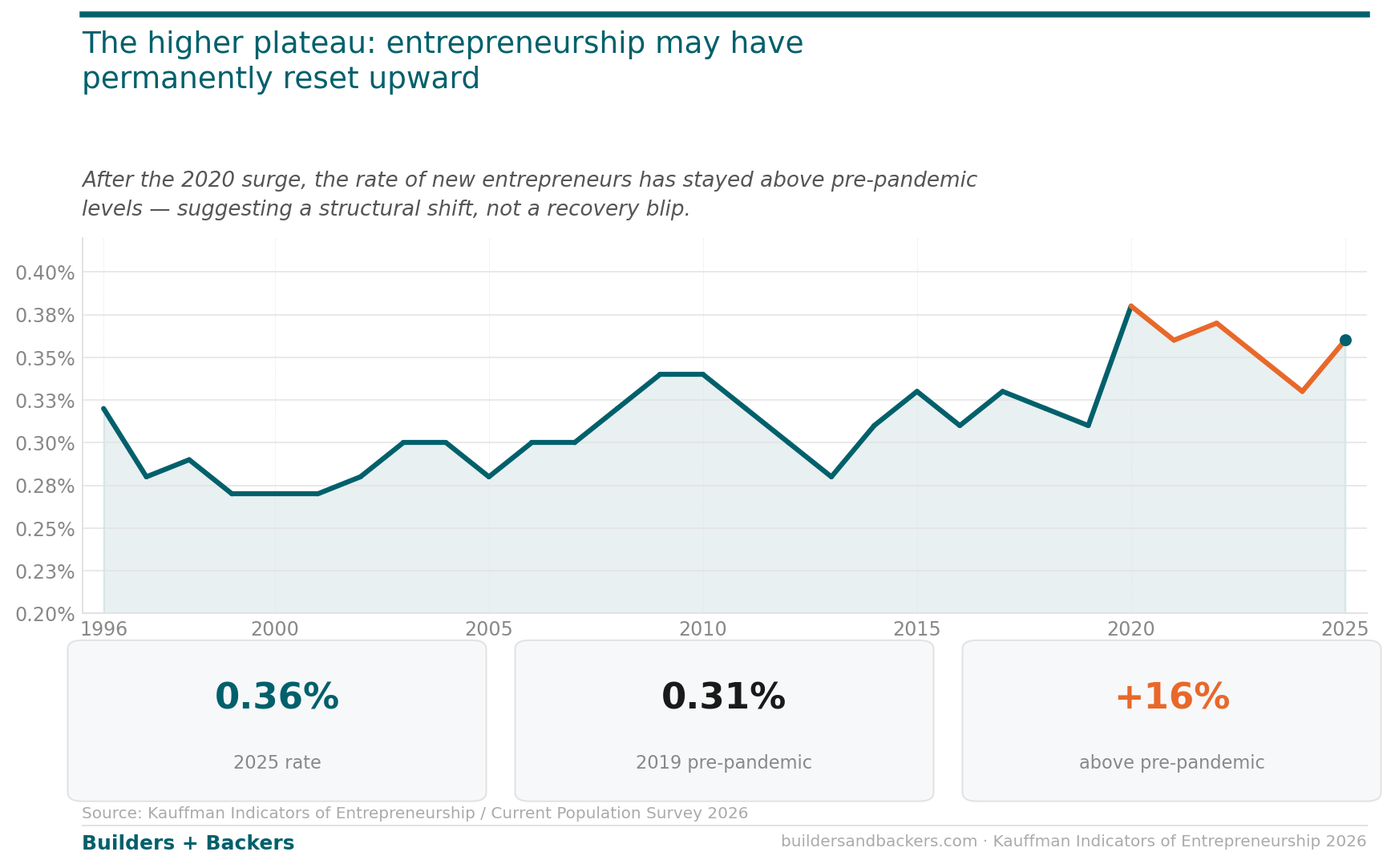

According to Kauffman’s newest indicators, the rate of new entrepreneurs in 2025 remains 16% above pre-pandemic levels. This no longer looks like a temporary post-COVID spike. It looks like a structural reset.

More Americans than ever are choosing — or needing — to build something of their own. That should be good news!

But buried in the same dataset is a much more complicated story. Because while startup formation is rising, the economic impact per startup appears to be falling. And that should force a serious rethink of what kind of entrepreneurship economy we are actually building.

More Founders, Less Impact

For fifteen years, the startup economy operated on a relatively stable assumption: More startups = more jobs

But the newest Kauffman data suggests that relationship is weakening.

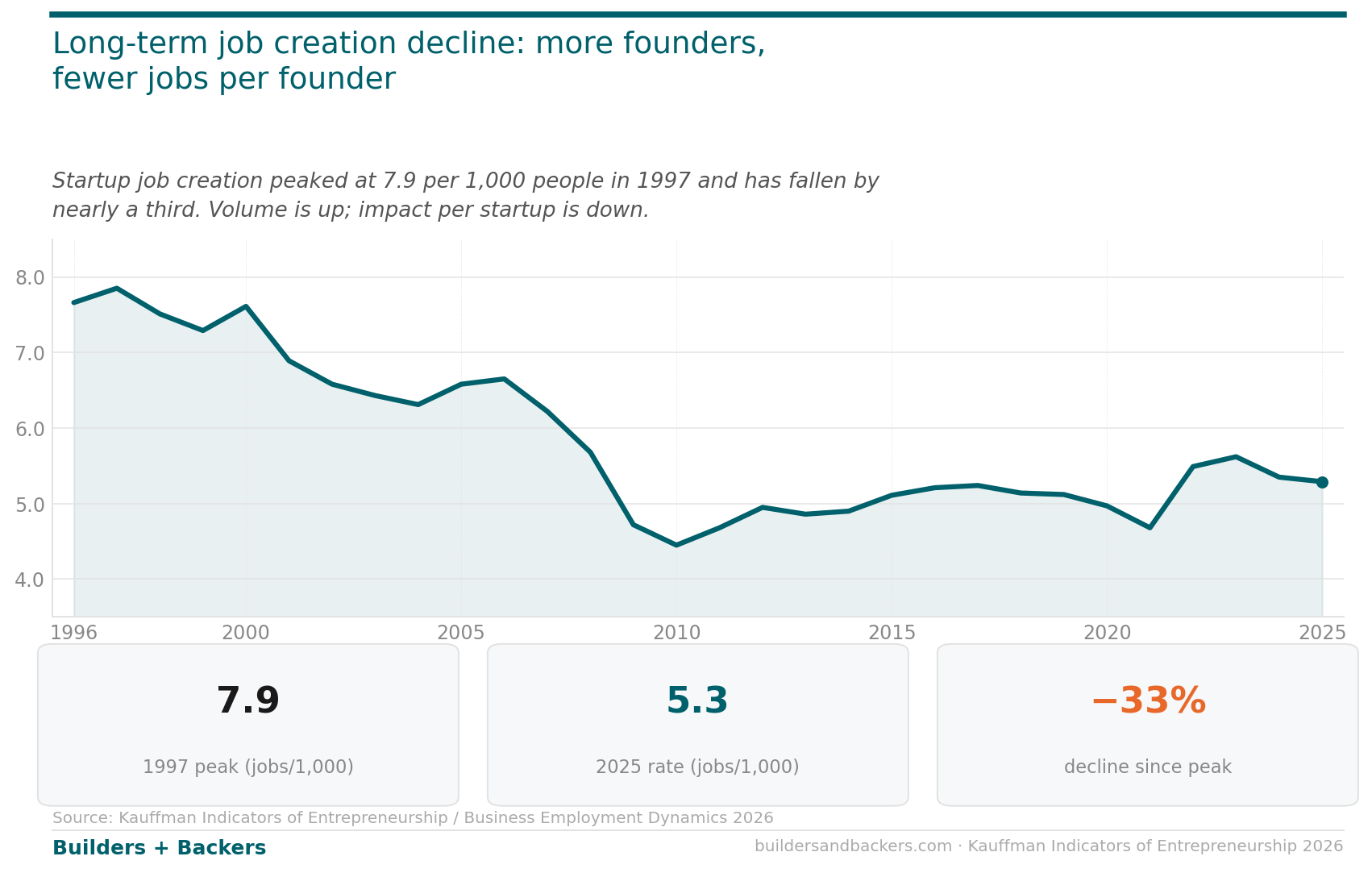

Yes, we have more founders. But we’re producing fewer jobs per founder. Startup job creation peaked in 1997 at 7.9 jobs per 1,000 people. In 2025, that figure sits at 5.3 — a decline of roughly one-third. And that's before we start seeing the full impact of AI.

Increasingly, entrepreneurship may be functioning not only as a pathway to company creation, but also as a form of economic adaptation: building careers and piecing together income from freelancing, side income, self-employment, contract work, and greater autonomy in a more fragmented labor market.

Many of these new businesses may never have been designed to become employer firms at all.

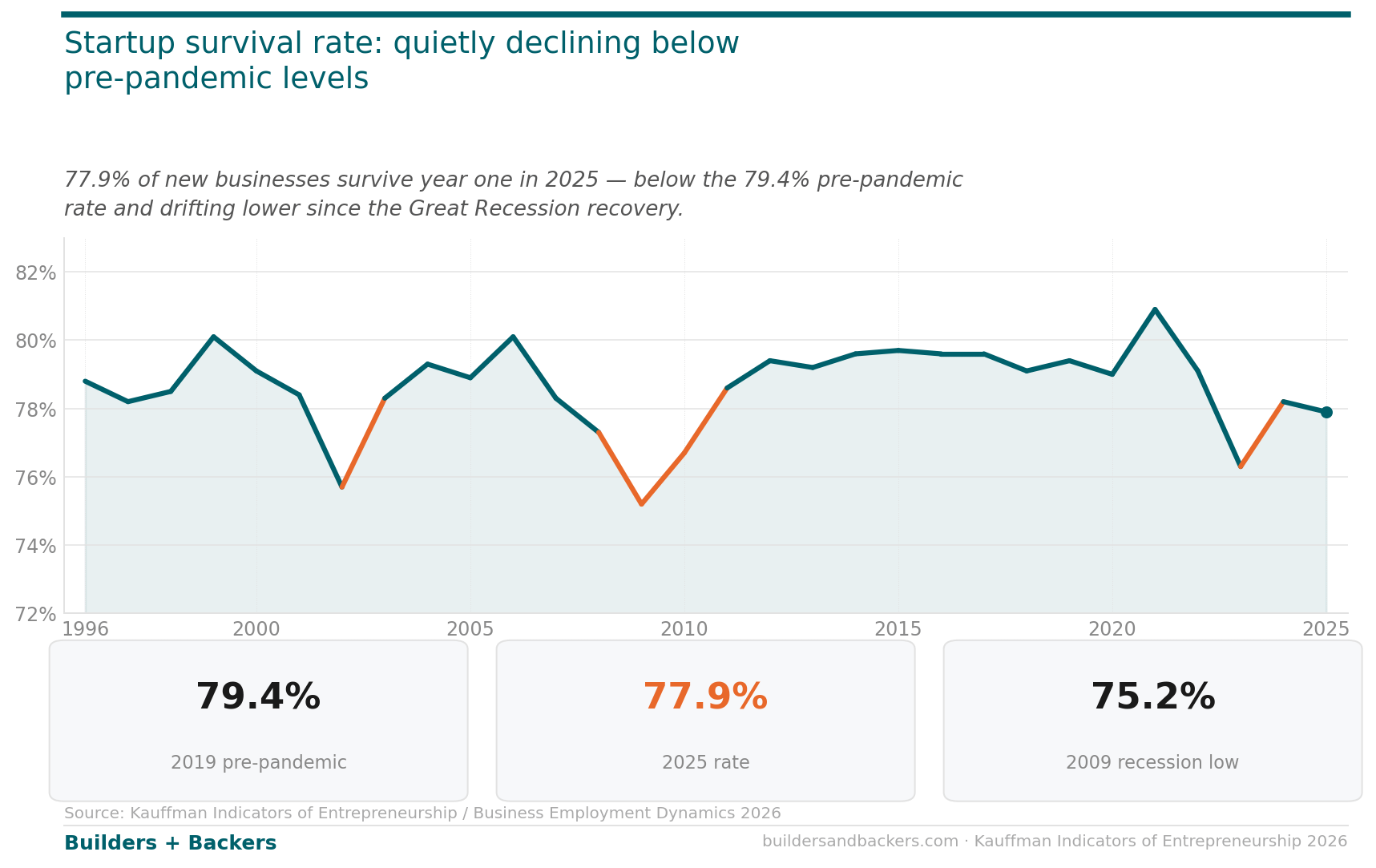

Startup survival rates are also moving in the wrong direction. In 2025, only 77.9% of startups survive their first year — below pre-pandemic levels and drifting downward since the post–Great Recession recovery.

All of this creates a fundamentally different economic equation than the one policymakers and ecosystem builders organized around in the 2010s.

If each startup creates fewer jobs than previous generations of startups, the economy now requires exponentially more startup formation just to maintain the same employment impact.

And if more of those startups fail earlier, the result is not necessarily greater economic dynamism.

It may simply be greater entrepreneurial churn.

The Ecosystem We Built. The Economy We Got

The original startup ecosystem movement was built around a relatively specific model of entrepreneurship: high-growth, tech-centric, venture-scalable, investor-backed.

That model generated enormous innovation, wealth creation, and technological acceleration.

But over time, the ecosystem became optimized for a narrower definition of entrepreneurial success: outsized venture returns. And that matters because economic systems produce what they are designed to reward.

While entrepreneurship broadened across America, capital concentrated at the top. In other words, the entrepreneurship economy diversified while the startup financing system consolidated.

Today, venture funding flows disproportionately to a tiny number of companies, founders, and regions. Massive rounds cluster around late-stage firms. AI investment is accelerating the concentration even further. Fewer funds control more capital. Fewer startups capture more attention.

At the exact same moment, the actual entrepreneurship economy is becoming broader, more distributed, and more demographically diverse than the infrastructure designed to support it.

Kauffman’s newest data makes that mismatch impossible to ignore.

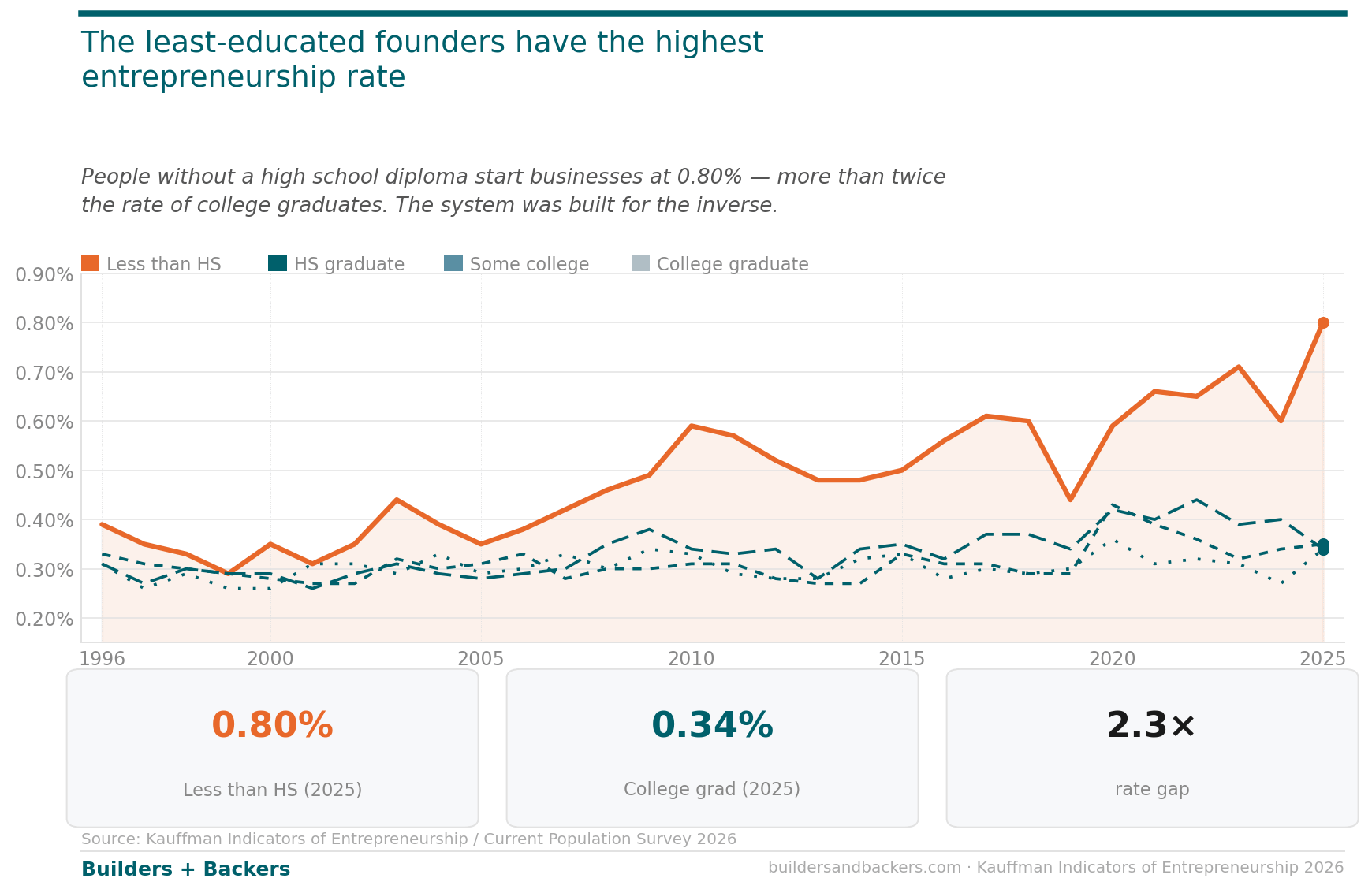

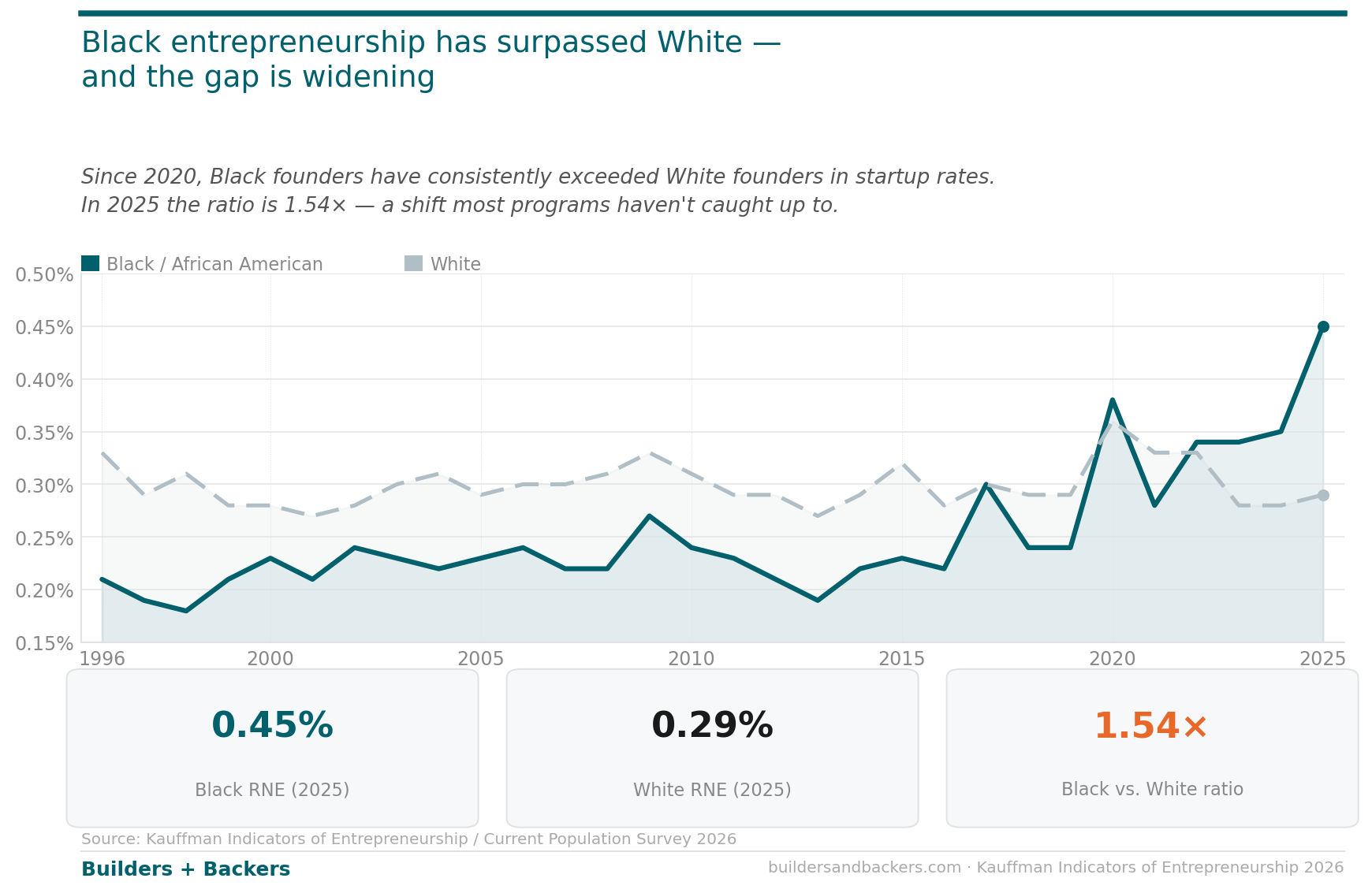

People without a high school diploma now start businesses at more than twice the rate of college graduates.

Black entrepreneurship rates now exceed White entrepreneurship rates — and the gap is widening.

These trends do not signal weaker entrepreneurship. In many cases, they may reflect populations responding fastest to economic disruption, labor market instability, and changing pathways to opportunity.

This is an ecosystem-defining shift.

But much of the startup support system still implicitly targets the inverse: credentialed founders, coastal networks, venture-scale trajectories, and businesses built for institutional capital.

The entrepreneurship economy expanded. The startup ecosystem specialized.

Those are no longer the same thing.

The Entrepreneurship Economy Has Changed

The most important takeaway from the new Kauffman data is not that entrepreneurship is weakening.

It’s that entrepreneurship is changing.

The United States may be entering an era where entrepreneurship is more common, more necessary, and more broadly distributed than at any point in modern history.

But the institutions built to support entrepreneurship still largely reflect the assumptions of the 2010 startup boom:

concentrated capital

venture-scale expectations

credentialed founders

hyper-growth models

a narrow definition of success

That mismatch is becoming increasingly visible in the data.

More people are starting businesses.

But fewer businesses appear to be scaling into durable employer firms.

Survival rates are softening.

And the pathways from startup formation to broad-based economic impact appear less certain than they once did.

That does not mean the original Kauffman thesis was wrong. Startups still matter enormously. But it may mean we drew the wrong conclusion from it.

We spent fifteen years building systems designed to increase startup formation. The next fifteen years may require systems designed to increase entrepreneurial durability, adaptability, and local economic resilience.

Because the question is no longer simply: “How do we create more startups?”

It’s: What kind of entrepreneurship economy are we actually optimizing for?

Check out Builders Studio. We can help anyone turn their entrepreneurial dreams and ideas into real, thriving companies.

If you’re an ecosystem leader, economic developer, or lead an organization supporting entrepreneurs and want to explore partnership, let’s talk.

I saw this from Ted Veile’s Substack and it aligns with what we’re seeing in Tucson. If we’re moving from job creation to value creation, then how can we support founders (of which I’m one so it matters to me) in how they pursue value?

we see the same concentration in crypto. last week 21 disclosed rounds = $467M, but $230M of that went to just three names. the long tail is hundreds of pre-seeds at $300k–$2M that nobody talks about